Everything you need to know about your 401k contribution Limits 2018. Most families don’t have the advantage of multiple tax sheltering opportunities. A small business, a farm, or nine children are available to only a few, so tax reducing techniques may difficult to come by. As a result, perhaps the single greatest tax sheltering device that most families possess today is their 401k retirement plan.

In this article, we will discuss 2018 contribution limits. (Related: 401k contribution limits for 2019). We will also assess 401k catch-up contributions and 401k matching rules.

401k Max Contributions

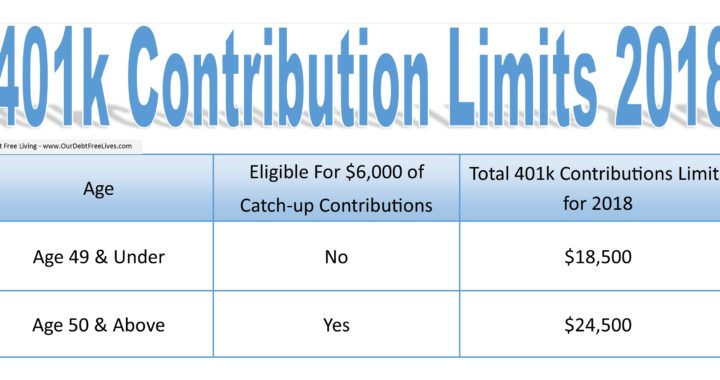

For 2018 the 401k limits are set at $18,500. This is the maximum annual 401k contribution allowed by law. This is a figure that has climbed 65% from $10,000 in 1999, thereby allowing participants to have larger retirement plan tax deductions than ever.

401k contribution limits 2018 will remain the same as in 2017. With 2018 contribution limits now attached to certain inflation indexes, the IRS and Treasury departments have determined that there will be no increase in 2018 maximum contributions. Many experts were expecting a decrease of 2018 401k contribution limits, primarily because of the somewhat deflationary environment we currently find ourselves in. It is important to note that all future adjustments will also be tied the same index. Check out our article on the rules for 401k distributions.

401k Catch-Up Contributions

In addition to the above, 2017 401k catch-up contributions are $6,000. The 401k catch-up gives participants 50 years old and older the ability to sock away a little extra before retirement. The 2018 401k catch-up will also remain at $6,000. Future catch-up contributions will be indexed for inflation in the same way deferrals are currently.

401k Matching Rules

If you’ve been a part of a retirement plan recently, you may have lost your 401k match. Many businesses, both small and large, have simply found that cutting the retirement plan match makes sense to the ongoing health of the business. Employers are looking under every stone for ways to save money, and 401k matches are not immune.

A 401k match typically involves employer contributions to the employee’s account based upon the employee’s deferral. Many employers match dollar-for-dollar, where others contribute less, i.e. 50¢ on the dollar.

Employers are allowed by law to match up to 6% of the employee’s salary. For example, if an employee makes $50,000 per year, the maximum employer match to the employee’s 401k account would equal $3,000. For those of you who are self employed read about the safe harbor 401k plan!

401k Contribution Limits 2018 Summary

- 401k contribution limits for 2017 and 401k contribution limits for 2018 are set at $18,000 and $18,500 respectively.

- Catchup contributions for 2017 and 2018 are set at $6,000.

- 401k Matching rules allow for matching up to 6% of the employee’s salary.