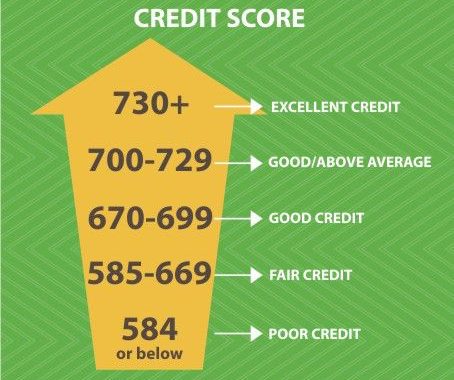

Are you ready to improve your credit in 5 easy steps? You may be thinking “Improve your credit in 5 easy steps? I have bad credit… Is this applicable to me? Will this work?” Yes! Improving your bad credit score is possible with very little effort. Let’s get started on improving your credit score!

Improve Your Credit In 5 Easy Steps

1. Improve your payment history:

This one is obvious but is so central to restoring a good credit rating that it merits mentioning. There are some simple steps that you can take to help you maintain a timely payment history. Write the due date on the front of the envelope. Just the mere act of writing the date down will help formulate it in your mind and elevate its prominence. Set a specific time each month for paying bills, for example, the second and forth Sunday of each month. By setting aside a time devoted to paying your bills you will avoid a payment slipping your mind. This is another benefit of using online banking for scheduling payments. This way is that it will be easier to set and meet your personal budget. Pay by automatic electronic transfer or by going online. If possible have a reminder sent to you by email, most companies now offer this service and many do it by default.

2. Reduce the amount you owe:

Keeping balances low on revolving credit is very important. The higher the percentage of the balance you owe versus your available credit the worse it is for your FICO score. Try to keep your balances at 10% or less of your available credit. Reducing the amount you owe will also reduce your monthly payments, which will make it easier for you to make timely payments. Transferring your account balances to credit cards with lower interest rates is certainly helpful but remember that paying off debt rather than just moving it around is always preferable.

3. Keep your “length of credit” high:

The higher the average age of your accounts is the better. With all other factors being equal an account that you have maintained for ten years will have a greater positive effect on your credit score than an account which you have had for only one year. Also, keep in mind that if you open too many new accounts all at once the average age of your accounts will drop, which will lower your score.

4. Apply for new credit within a confined time period:

When applying for new credit, if you submit multiple applications to different sources do so in a short period of time, this way they will all be counted as a search for one single loan. If you spread the applications out over an extended period of time they will appear as separate loan inquiries, which will have a negative impact on your score.

5. Maintain a small number of credit cards:

If you presently do not have any credit cards try to obtain a limited amount of credit cards and make timely payments on them. Having no credit cards at all will have a negative impact on your FICO score. If need be, set up a secured credit card or two. They are very easy to obtain, as they are seen as having an extremely low risk from a bank’s perspective.